Posted on GoogleTrustindex verifies that the original source of the review is Google. Rick contacted me out of the blue one day because he saw all of the properties I was buying in the Philly area. I gave him a shot to refi one of my single family rentals. I was surprised how smooth the deal went. Lived up to everything he promised. I will def use him again for future DSCR loans.Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Nonbank Clearing was excellent due to Rick Bagel. He was informative and efficient. He was able to get me answers expeditiously. I was able to close on my loan in the allotted timeframe he gave me. He showed for closing and made sure everything went smoothly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Working with Nonbank Clearing for my cash-out refi deal was a great experience. Specifically, working with Rick made the entire process easy and straightforward. He was incredibly detailed in his explanations, and I found their interest rates to be competitive, which was a huge plus. What really stood out was that it felt like a true partnership; he provided me with multiple options and walked me through the pros and cons of each. His clear and direct communication made the process feel transparent and efficient, and I felt like I was getting a good deal. I would highly recommend Nonbank Clearing!Posted on GoogleTrustindex verifies that the original source of the review is Google. Rick was helping me with the loan so quickly, smooth and really professional . I will be back with him for the next loan . 5 stars I recommendedPosted on GoogleTrustindex verifies that the original source of the review is Google. Working with Rick was truly a game changer! I came to him with a sticky home situation in NJ and wasn’t sure there was even a path forward but Rick made the impossible happen. He not only secured me a fantastic loan, but did so with a level of dedication and professionalism that’s incredibly rare in the lending world! Rick is extraordinarily responsive, transparent, and genuinely invested in helping his clients succeed. He took the time to understand my goals, walked me through every step, and made a stressful process feel manageable....even exciting. :D A year later, I still recommend him to everyone I know & talk about that time. :) If you’re looking for someone who is knowledgeable, reliable, and will go the extra mile (and then some), Rick is totally your guy. You won’t find better! (Promise!)Posted on GoogleTrustindex verifies that the original source of the review is Google. Rick help me secure a DSCR loan for a rental property in NH. The transaction was smooth and Rick helped in every step along the way. I'll be using him again.Posted on GoogleTrustindex verifies that the original source of the review is Google. Great rates and very fast closing. Rick is the best!Posted on GoogleTrustindex verifies that the original source of the review is Google. Rick is incredibly knowledgable. He helped me purchase an investment property. I'll be using him for many more transactions.Posted on GoogleTrustindex verifies that the original source of the review is Google. I have worked with Rick a handful of times with a customers refinancing of several investment properties. He has always been professional and very easy to work with, I would highly recommend Rick and his team.Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Nonbank Clearing has been nothing but professionalism with no unforeseen changes in the process and a smooth closing on my refinance. I would recommend this team without reservation for your real estate financing needs.

Full Doc Bank Loan Tear Sheet

| Loan Amount | $200k minimum. No firm maximum. |

| Loan Term and Amortization | 5–20 year term with 20–25 year amortization. |

| Coverage Area | Greater Philadelphia |

| Interest Rates, Points and Fees | Lowest available |

| Borrower Income and Asset Verification | Complete asset verification, 24 months business and personal bank statements, and last two years business and personal tax returns. |

| Entity (LLC or Inc) vs. Individual Name Vesting | Both allowed |

| Credit Scoring for Multi Member LLC | Lender will pull credit for every Member owning 10–20% or more. |

| Purchase LTV | 65–80% of purchase price |

| Refinance LTV | 65–75% of appraised value |

| Property Level Cash Flow | 1.20–1.30 DSCR at 20–25 year amortization |

| Seasoning Requirement for Cash Out Refi | 6–24 months with property level income seasoning |

| Monthly Payment | Principal + Interest payment, with property taxes and insurance paid separately. |

| Eligible Property Types | Most property types eligible |

| Timeline to Close | 45–90 days |

Commercial Bank Term Loan Calculator

Bank loans for multifamily and commercial property are full doc loans, meaning they require 2 years personal and business income history, and the bank will verify assets (e.g. cash, stock, retirement plans, and other real estate owned). Unlike DSCR loans, banks typically do not escrow for property taxes and property insurance, so the monthly payment is just Principal and Interest (PI), as opposed to a DSCR loan payment which is Principal, Interest, Taxes, and Insurance (PITI). Typical amortization terms for bank loans are 20 years (240 months) and 25 years (300 months).

Up Front Costs

Full Doc Bank Loan Process

Step 1- Initial Discussion, Loan Application, and Term Sheet

- Discuss the purchase or refi scenario and property level details

- Suggest relevant loan programs and provide parameters

- Loan application and initial info request (we can get this over the phone too)

- Term Sheet and Appraisal Fee

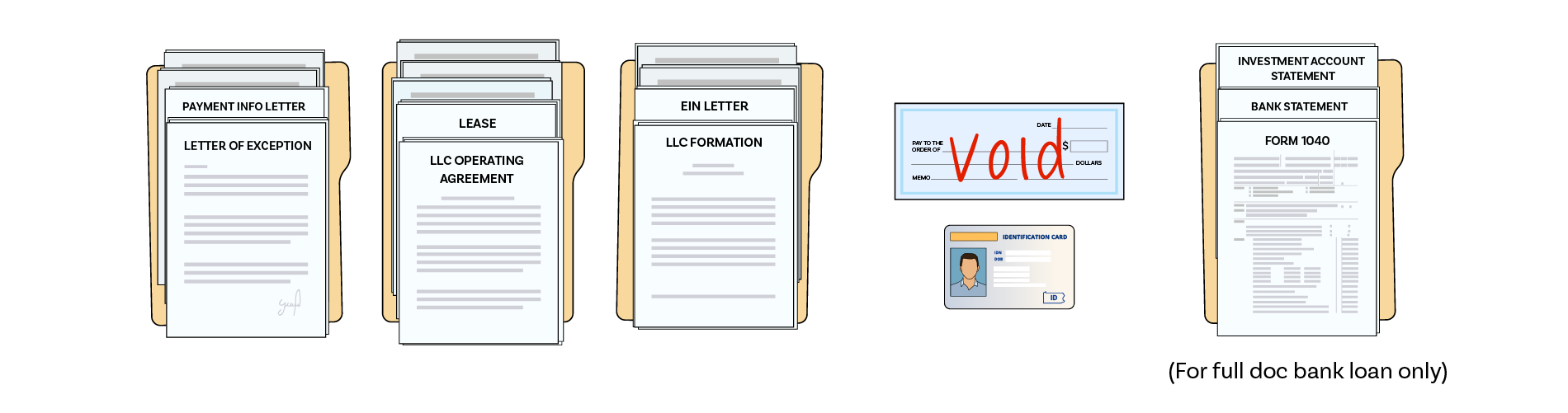

Step 2- Initial Info Required for Full Doc Bank Loan

- Any remaining info points to complete the Loan Application

- Photo of ID and void check

- Contact information for your title agent and insurance agent

- If borrower is an LLC, then LLC Operating Agreement and EIN Letter

- Bank statements with cash to close and required reserves for Purchases

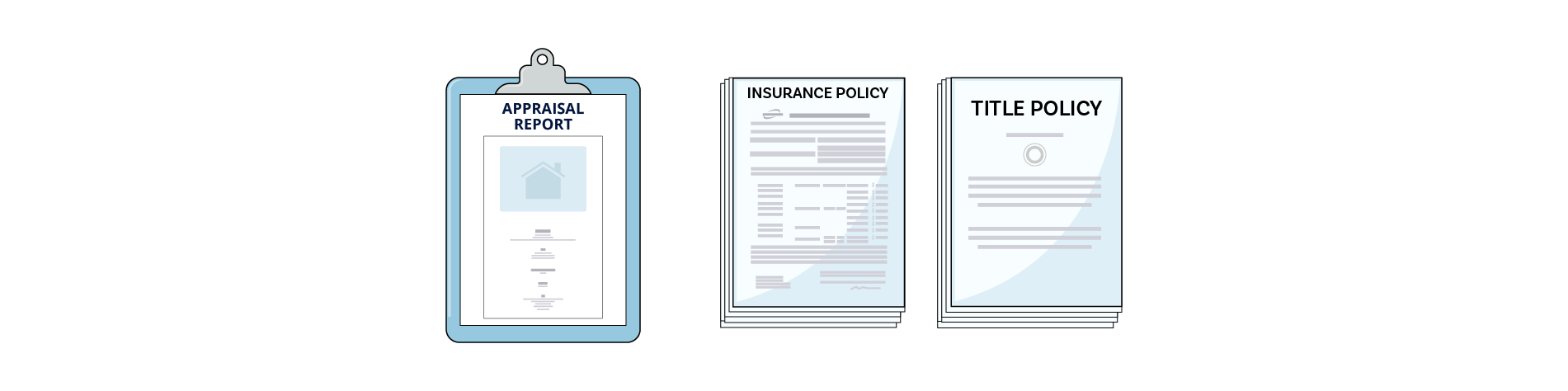

Step 3- Appraisal, Title, Insurance, and Additional Info from Borrower

- Appraiser visits the property and completes the appraisal report

- Lender reviews the appraisal report, internally re-checks value and reviews for property condition

- Title agent provides title policy, works with lender on revisions and clarifications

- Insurance agent provides insurance policy, works with lender on revisions and clarifications

- Last Two Years Business and Personal Bank Statements

- Investment Account Statements

- Documentation as needed for other real estate owned

- Bank Statements for Income Verification

- Lender usually comes up with other things to ask for from borrower

Step 4- Final Underwriting, Closing, and Funding

- Lender sends complete file to underwriting, and they may find issues or require more things at that point

- Final coordination between title company and lender on loan docs and scheduling

- Closing and Funding

Full Doc Bank Term Loans Commentary

A full doc bank loan would adjust rental income downward for operating expenses and vacancy (not just taxes and insurance) and require 1.20 or 1.25 dscr at 20 or 25 year amortization. Full doc loans have more stringent debt service coverage guidelines than a DSCR loan for Commercial Property

Why work with a third party originator like Nonbank Clearing on a full doc bank loan?

We deal with banks that are better than average on service, timeline to close, structure, and pricing. We identify potential issues early in the loan process to avoid the dreaded denial notice after 1-2 months of work for a reason that could have been spotted earlier. We are not quick to switch lenders over something small, but we can pivot to another lender if we sense we are coming to a true impasse with a given bank. We can also help with the mountain of paperwork involved in a full doc loan application and loan process.

Nonbank Clearing Advantages

- Competitive rates and structures (multiple lender outlets)

- Familiar with bank underwriting and guidelines

- Excellent service and simplified loan processing