- No Seasoning

- No Occupancy

- No Income

- Competitive Rates

- Simplified Process

- Same Day Approval

DSCR loan for 1-4 unit residential is our most popular loan product. It is also known as the long term rental loan, ltr loan, and 30 year no doc rental loan. The no doc process, flexibility on seasoning, and rates, make DSCR loans a compelling alternative to full doc bank loans for 1-4 unit residential rental properties.

Testimonials

Posted onTrustindex verifies that the original source of the review is Google. Rick contacted me out of the blue one day because he saw all of the properties I was buying in the Philly area. I gave him a shot to refi one of my single family rentals. I was surprised how smooth the deal went. Lived up to everything he promised. I will def use him again for future DSCR loans.Posted onTrustindex verifies that the original source of the review is Google. My experience with Nonbank Clearing was excellent due to Rick Bagel. He was informative and efficient. He was able to get me answers expeditiously. I was able to close on my loan in the allotted timeframe he gave me. He showed for closing and made sure everything went smoothly.Posted onTrustindex verifies that the original source of the review is Google. Working with Nonbank Clearing for my cash-out refi deal was a great experience. Specifically, working with Rick made the entire process easy and straightforward. He was incredibly detailed in his explanations, and I found their interest rates to be competitive, which was a huge plus. What really stood out was that it felt like a true partnership; he provided me with multiple options and walked me through the pros and cons of each. His clear and direct communication made the process feel transparent and efficient, and I felt like I was getting a good deal. I would highly recommend Nonbank Clearing!Posted onTrustindex verifies that the original source of the review is Google. Rick was helping me with the loan so quickly, smooth and really professional . I will be back with him for the next loan . 5 stars I recommendedPosted onTrustindex verifies that the original source of the review is Google. Working with Rick was truly a game changer! I came to him with a sticky home situation in NJ and wasn’t sure there was even a path forward but Rick made the impossible happen. He not only secured me a fantastic loan, but did so with a level of dedication and professionalism that’s incredibly rare in the lending world! Rick is extraordinarily responsive, transparent, and genuinely invested in helping his clients succeed. He took the time to understand my goals, walked me through every step, and made a stressful process feel manageable....even exciting. :D A year later, I still recommend him to everyone I know & talk about that time. :) If you’re looking for someone who is knowledgeable, reliable, and will go the extra mile (and then some), Rick is totally your guy. You won’t find better! (Promise!)Posted onTrustindex verifies that the original source of the review is Google. Rick help me secure a DSCR loan for a rental property in NH. The transaction was smooth and Rick helped in every step along the way. I'll be using him again.Posted onTrustindex verifies that the original source of the review is Google. Great rates and very fast closing. Rick is the best!Posted onTrustindex verifies that the original source of the review is Google. Rick is incredibly knowledgable. He helped me purchase an investment property. I'll be using him for many more transactions.Posted onTrustindex verifies that the original source of the review is Google. I have worked with Rick a handful of times with a customers refinancing of several investment properties. He has always been professional and very easy to work with, I would highly recommend Rick and his team.Posted onTrustindex verifies that the original source of the review is Google. My experience with Nonbank Clearing has been nothing but professionalism with no unforeseen changes in the process and a smooth closing on my refinance. I would recommend this team without reservation for your real estate financing needs.

What is a DSCR Loan?

- For 5+ unit residential (multifamily), mixed use, and commercial property types, please refer to the dscr loan programs on the multifamily and commercial and mixed use loan pages

How to Qualify for a DSCR Loan

DSCR Loan Calculator

Almost all DSCR loans are 30 year term, so we’ve plugged in 360 months for the term length.

For 1-4 unit residential, multifamily, and commercial / mixed use DSCR loans, the lenders escrow the estimated monthly cost for property taxes and property insurance. The monthly payments are PITI (Principal + Interest + Taxes + Insurance), like a 30 year home loan, even though these are commercial loan products.

Up Front Costs

In choosing a DSCR lender, rates, points, and fees are important, but equally important are service, reliability, and not finding a lender that bids low to win loans and re-trades later.

DSCR lenders have less stringent dscr criteria than bank lenders. DSCR loans for 1-4 unit residential properties do not require leases or occupancy, and lenders can go off market rate for rents. DSCR loans for multifamily, mixed use, and commercial, typically require 70% occupancy. The usual dscr requirement for a DSCR loan is 1.00, based on rents divided by the PITI monthly payment with 30 year amortization, and we have lenders that can work with 0.75-0.99 dscr for certain scenarios. A full doc bank loan would adjust rental income downward for operating expenses and vacancy (not just taxes and insurance) and require 1.20 or 1.25 dscr at 20 or 25 year amortization.

DSCR Loans vs. Hard Money Loans

| DSCR Loan | Hard Money Loan | |

|---|---|---|

| Rates, points and fees | Near bank rates with good FICO score | Higher rates and points |

| Property needs repairs | Can’t close a DSCR loan with any non-cosmetic repairs needed or any safety issues | Loan includes a rehab budget |

The above is the story short on DSCR loans vs. Hard money loans. DSCR loans are to buy or refinance properties that are already rent ready without any property condition issues. Hard money loans are used to buy properties that need work. DSCR loans are popular to refinance hard money loans once a rehab project is completed.

DSCR Loan Process

Step 1- Initial Discussion, Loan Application, and Term Sheet

- Discuss the loan scenario

- Suggest relevant loan programs and provide parameters

- Loan application and initial info request (we can take this over the phone too)

- Term Sheet and Appraisal Fee

Step 2- Initial Info Submittal for DSCR Loan

- Loan Application and Appraisal Fee (see previous step)

- Photo of ID and void check

- Contact information for your title agent and insurance agent

- If borrower is an LLC, then LLC Operating Agreement and EIN Letter

- If any units are leased, then copy of the leases

- If purchase, or refi without cash out, bank account with cash to close and required reserves

- No deposit verification needed for cash out refi

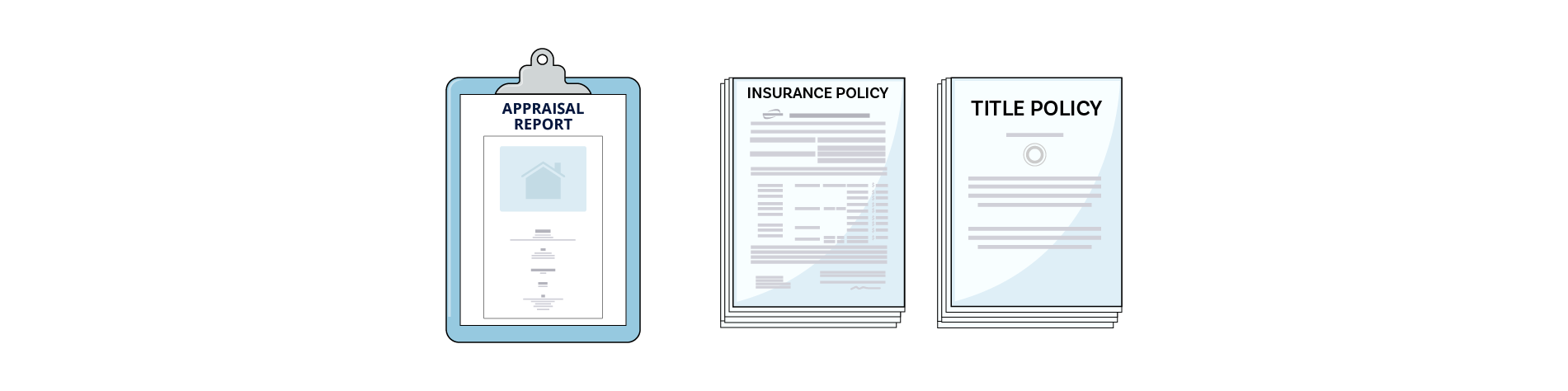

Step 3- Appraisal, Title, Insurance, and Additional Info from Borrower

- Appraiser visits the property and completes the appraisal report

- Lender reviews the appraisal report, internally re-checks value, and reviews appraisal report for property condition issues

- Title agent provides title policy, works with lender on revisions and clarifications

- Insurance agent provides insurance policy, works with lender on revisions and clarifications

- Lender usually comes up with other things to ask for from borrower

Step 4- Final Underwriting, Closing, and Funding

- Lender sends complete file to underwriting, and they may find issues or require more things at that point

- Final coordination between title company and lender on loan docs and scheduling

- Closing and Funding

DSCR Loan Requirements

Most of the requirements for DSCR loans are outlined in the graphic above. If you are getting your stuff together to apply for a DSCR loan, please be ready to meet the following requirements:

- Loan Application

- LLC documents including Operating Agreement

- Title Policy meeting lender requirements

- Insurance Policy meeting lender requirements

- Leases (if you have any leases)

- Purchase contract (if purchase)

- HUD1 from purchase (if purchased recently)

- Completed appraisal (ordered by lender, paid for by borrower)

- No investor experience required

- No income verification required

All loans are subject to credit approval. These requirements are intended to be a summary and not supposed to be comprehensive. Lenders usually ask for more stuff.

DSCR Loan vs. Bank Loan vs. Conventional Loan

| DSCR Loan for 1-4 unit residential rental | Commercial Bank Loan for 1-4 unit residential | Conventional Loan for 1-4 unit rental | |

|---|---|---|---|

| Seasoning Requirement (for refi) | 0 days for up to 100 LTC, 90 days for full LTV refi | 6-12 months for cash out refi | 12 months for cash out refi |

| Borrower Income, Debt to Income Ratio (DTI ratio) Requirement | None. This is a no income rental mortgage. | 50% outside debt to income ratio | 50% outside debt to income ratio |

| Asset Requirements (Cash Out Refi) | None | Full asset verification | Full asset verification |

| Asset Requirements (Rate and Term Refi) | 6 months payments in the bank | Full asset verification | Full asset verification |

| Asset Requirements (Purchase) | Cash to close + 6 mo payments in the bank | Full asset verification | Full asset verification |

| Time to Close | 20-30 days | 40-60 days | 30-40 days |

| Occupancy Requirement | No lease or occupancy requirement | Leases required | Leases required |

| Interest Rates, Points, and Fees | Same or slightly higher than conventional, or commercial bank | Sometimes better than conventional, sometimes the same | Same or slightly higher than commercial bank loan |

| FICO requirements | 720+ for best rates, 660-719 for ok rates, 580-659 at higher rates | 620-680+ | 620+ |

| Loan Term | 30 year | 5, 20, 25, or 30 year | 15 or 30 year |

DSCR Loan Pros and Cons

| DSCR Loan Pros | DSCR Loan Cons |

|---|---|

| No seasoning requirement for cash out refi | Sometimes nominally higher interest rate, points / fees, and prepayment penalty |

| No debt-to-income (DTI) ratio or borrower level income requirements | DSCR lenders require full replacement cost coverage on hazard insurance, which can be more expensive than bank lender minimum coverage |

| Quicker process with fewer info requests and underwriter conditions | DSCR lenders can be sticklers on property condition items from appraisal report and require nominal repairs that full doc lenders overlook |

| Lenders can go off market rate for vacant finished units, and lenders have a lower DSCR benchmark (1.00 on 30 year amo) | DSCR lenders are less good about allowing addendums to be signed at closing - they like a complete file before closing |

| No limit on # of properties, Portfolio OK | For single family purchase, DSCR loans have a higher down payment requirement than home loan for investment property |

What is the highest LTV for DSCR loan?

| Loan Amount (Purchase or Refi) | $75k-$3mm per property |

| Purchase |

80% of purchase price (higher rate) * 75% of purchase price (better rate) * * cash to close = % of purchase price + buyer paid closing costs + tax and insurance escrows |

| Rate and Term Refinance (e.g. repay existing term loan or repay construction bridge loan) |

80% of appraised value (700+ fico) 75% of appraised value (680+ fico) 65% of appraised value (580-679 fico) |

| Cash Out Refinance |

75% of appraised value (680+ fico) 75% of appraised value (650-679 fico) higher rate 65% of appraised value (580-649 fico) |

What are DSCR portfolio loans?

DSCR portfolio loans are a type of blanket loan that has 5 or more properties under 1 loan. DSCR portfolio loans are very similar to DSCR loans for individual properties, except the lender offer breaks on fees and points for it being a bigger loan. DSCR portfolio loans can be used for no doc portfolio purchase, portfolio rate and term refinance, or portfolio cash out refinance for 1-4 unit residential investment properties. DSCR portfolio loans are competitive against bank loans on seasoning, proceeds, and rates for no doc rental portfolio refi.

What are DSCR loans for Short Term Rentals?

DSCR loans can be used for Short Term Rentals. DSCR loans for short term rentals are also known as STR loans. They are similar to DSCR loans except lenders can go off Airdna ® market data to underwrite income as a short term rental. For short term rental loan refinances, the property must already be listed on Airbnb ®, VRBO ®, or with Realtor ® to verify that it is being used as a short term rental.

What are DSCR loans for Medium Term Rentals or Mid Term Rentals?

Medium term rentals include boarding houses, weekly rent, rent by the room, and anything that is between short term rental and a standard 6-12+ month residential lease. We have DSCR loans for medium term rentals. There are fewer DSCR lenders for this type of rental strategy and they have underwriting requirements in addition to usual DSCR loan requirements to meet this setup.

Are DSCR Loans for Individuals or only for LLCs?

We have DSCR loans for individuals, but in most states DSCR loans for LLCs are more competitively priced. Borrowers can also have the title company transfer a property from individual name to LLC name at the loan closing. Please check your local transfer taxes first. Here in Philadelphia, PA, the transfer tax rates are high. Other places don’t have transfer tax or they have very low transfer tax.

Do DSCR lenders go off the higher of two or three credit scores?

For an LLC with 2-3 owners, where each owner has an equal interest, our DSCR lenders can use the credit score of the member with the highest score. Generally, a DSCR loan is a loan made to an LLC, one LLC member is the primary applicant who signs most of the loan documents, and the remaining members sign a more limited set of documents including a personal guarantee.

Can I get a DSCR loan without a tenant?

Yes, you can get a DSCR loan without a tenant. No leases or occupancy is required for DSCR loans for 1-4 unit residential properties. All units must be in rent ready condition. If the properties are leased, then you need to provide copies of the leases. For DSCR purchase loans, lender can go off market rents from appraisal report instead of in place rents. For DSCR refi, lender will go off the lower of in place rents and market rent from the appraisal report.

Can I use DSCR loan for condo inventory or homebuilding inventory?

Yes, you can use DSCR loans as a condo inventory no doc refi or homebuilding inventory no doc refi. DSCR loans are an attractive and convenient option for recently completed construction refi. 20-30 days to close and rates near bank rates.

Are DSCR loans BRRRR loans?

DSCR loans can be part of a BRRRR strategy. BRRRR stands for “buy, rent, rehab, refinance, repeat”. DSCR loans are popular with Brrrr method investors because the loans allow brrrr investors to refinance and repeat quickly. In fact, the first “r” in brrrr, “rent” isn’t even required for 1-4 unit residential investment properties- you can close the refi with the units rent ready without leases or occupancy. No seasoning DSCR loans are a powerful tool for Brrrr investors.

More Information about DSCR Loans

DSCR loans are a type of mortgage for rental property. DSCR loans are loans for investment properties only. They are not allowed for properties where the owner lives. This avoids the moral issue of potentially needing to foreclose on someone’s personal residence, and being accused of putting someone in a loan on their own house that they cannot afford. The finance and lending businesses took a black eye in 2008 when the major banks were bailed out / given extensions by taxpayers, and regular people lost their homes to those same banks by foreclosure. The banks have since made changes to be more conservative and fairer for home loans, which is good. The private lending market has stepped up to serve investors. DSCR loans are especially competitive on cash out refi for investment property, and as an easy way to refinance rental property. DSCR cash out refi is a no doc refi- meaning there are no tax returns or borrower level income verification required- and it is also known as a 30 year no doc loan for investment property. DSCR loans are the best thing going for 1-4 unit residential investment property cash out refi. DSCR loans can be used for purchase or cash out refi on a single family home, duplex (2plex), triplex (3plex), or quadroplex (4plex) rental loan.

Nonbank Clearing Advantages

- Cover almost any lendable scenario (multiple outlets)

- Good service and simplified loan processing

- Competitive rates, structures, and seasoning

If your existing lender can refi as soon as you complete projects, you are not maxing on debt to income ratio requirements or maximum # of loans, and you have competitive service, timeline to close, and rates, then there is little benefit to switching to DSCR loans.

If you want a new lender that is competitive on seasoning, timeline to close, with no borrower level income requirements and no max # of loans, then give us a call and we’ll get you set up 609-468-9324.