Posted onTrustindex verifies that the original source of the review is Google. Rick contacted me out of the blue one day because he saw all of the properties I was buying in the Philly area. I gave him a shot to refi one of my single family rentals. I was surprised how smooth the deal went. Lived up to everything he promised. I will def use him again for future DSCR loans.Posted onTrustindex verifies that the original source of the review is Google. My experience with Nonbank Clearing was excellent due to Rick Bagel. He was informative and efficient. He was able to get me answers expeditiously. I was able to close on my loan in the allotted timeframe he gave me. He showed for closing and made sure everything went smoothly.Posted onTrustindex verifies that the original source of the review is Google. Working with Nonbank Clearing for my cash-out refi deal was a great experience. Specifically, working with Rick made the entire process easy and straightforward. He was incredibly detailed in his explanations, and I found their interest rates to be competitive, which was a huge plus. What really stood out was that it felt like a true partnership; he provided me with multiple options and walked me through the pros and cons of each. His clear and direct communication made the process feel transparent and efficient, and I felt like I was getting a good deal. I would highly recommend Nonbank Clearing!Posted onTrustindex verifies that the original source of the review is Google. Rick was helping me with the loan so quickly, smooth and really professional . I will be back with him for the next loan . 5 stars I recommendedPosted onTrustindex verifies that the original source of the review is Google. Working with Rick was truly a game changer! I came to him with a sticky home situation in NJ and wasn’t sure there was even a path forward but Rick made the impossible happen. He not only secured me a fantastic loan, but did so with a level of dedication and professionalism that’s incredibly rare in the lending world! Rick is extraordinarily responsive, transparent, and genuinely invested in helping his clients succeed. He took the time to understand my goals, walked me through every step, and made a stressful process feel manageable....even exciting. :D A year later, I still recommend him to everyone I know & talk about that time. :) If you’re looking for someone who is knowledgeable, reliable, and will go the extra mile (and then some), Rick is totally your guy. You won’t find better! (Promise!)Posted onTrustindex verifies that the original source of the review is Google. Rick help me secure a DSCR loan for a rental property in NH. The transaction was smooth and Rick helped in every step along the way. I'll be using him again.Posted onTrustindex verifies that the original source of the review is Google. Great rates and very fast closing. Rick is the best!Posted onTrustindex verifies that the original source of the review is Google. Rick is incredibly knowledgable. He helped me purchase an investment property. I'll be using him for many more transactions.Posted onTrustindex verifies that the original source of the review is Google. I have worked with Rick a handful of times with a customers refinancing of several investment properties. He has always been professional and very easy to work with, I would highly recommend Rick and his team.Posted onTrustindex verifies that the original source of the review is Google. My experience with Nonbank Clearing has been nothing but professionalism with no unforeseen changes in the process and a smooth closing on my refinance. I would recommend this team without reservation for your real estate financing needs.

New Construction Loan Tear Sheet

| New Construction Loan | |

|---|---|

| Loan Amount | $150k min. No firm max. |

| Loan Term | 12–24 months |

| Coverage Area | Most States |

| Max Leverage | 80 - 90% of purchase price + construction hard cost |

| Time to Close | 20 - 30 days |

| Borrower Income and Asset Verification, DTI | No |

| Lender Imposed Maximum # of Projects | No |

| Property Types | Ground up construction of 1 or multiple 1–4 unit houses or townhomes for sale or for rent |

| Mid Project Refi | Allowed |

| Build to Rent Strategy | Allowed |

| Teardown Strategy | Allowed |

| Rates, Points and Fees | Private bridge rates |

| Experience Required | Yes |

| Liquidity Required | Yes |

| Monthly Payment | Interest only |

| Balloon Payment | Pay back the loan balance at sale or refinance |

| Minimum Interest | No minimum interest |

| Interest Charged on Undrawn Amounts | No interest on undrawn amounts |

| LTARV Requirement | 70–75% LTARV, meaning the loan amount can be no more than 70–75% of the as complete value |

Nonbank New Construction Loan Experience Requirements

Private lenders all require investment experience, but not necessarily previous ground up construction experience. There is no firm minimum experience requirement for 1st time ground up construction loan. Below are a few marginal experience scenarios where we’ve won loan approvals for our clients:

Nonbank New Construction Loan Experience Requirements

| Borrower Experience Profile | New Construction Loan Approved |

|---|---|

| 1 ground up completed for personal residence + 1 rehab completed and rented as an investor | ✅ New construction mid project refi |

| 1 ground up completed and sold as an investor without using any loans | ✅ New construction bridge purchase |

| 3 rehabs completed and sold as an investor and 2 rentals held that borrower had rehabbed | ✅ New construction bridge purchase |

| Several new construction homes for clients with builder name on the building permits. | ✅ New construction bridge purchase |

New Construction Mid Project Refi Notes

Nonbank Clearing specializes in mid project refinances. Typically, these scenarios arise when a borrower attempts a project all cash, and wants a loan to complete the project, or they have a construction loan that has either come due or doesn’t have enough rehab budget to complete the project. We are not magicians, but if a mid-project refi is doable, then we want to help execute.

New Construction Mid Project Refi Notes

| ✅ Mid Project Refi Good Looks | ❌ Mid Project Refi Not So Good Looks |

|---|---|

| ✅ No debt, little debt, or moderate debt on the property | ❌ Project is already overleveraged |

| ✅ Recently sold nearby similar homes to support as complete value of the project | ❌ No resale or new construction similar homes sold recently nearby to support value projection |

| ✅ Borrower has investment experience outside of this project | ❌ Borrower has no investment experience outside of this project |

| ✅ Borrower has receipts for at least some of the work already completed | ❌ Borrower has no receipts for any of the work completed |

| ✅ Borrower has 700+ FICO score or at least high 600s FICO score | ❌ Borrower has low FICO score |

| ✅ Borrower is current with existing lender | ❌ Borrower is past due on a hard money loan |

| ✅ Borrower has the required plans and permits | ❌ Borrower still does not have the permits needed to finish the work |

| ✅ Borrower has a scope of work and breakdown for the remaining project cost | ❌ Borrower does not know what it is going to cost to complete the project |

New Construction Loan Calculator

Fix n flip loans and New construction loans are typically 12 month, 18 month, or 24 month balloon loans, interest only, where the borrower intends to repay the loan by either refinancing (taking out) the bridge loan with a permanent loan, or selling the property and repaying the loan at sale.

The "Rehab Holdback Use Factor" is a simplification to help estimate the total monthly interest payments. Our lenders typically don't charge interest on undrawn amounts, so we've included this percentage to adjust for not using the entire rehab holdback amount from the beginning of the loan. Our lenders typically have no minimum term length. They get you on the up front points and fees and then the total interest paid is variable depending on how soon you draw the money and how many months until you pay it back, with no minimum interest.

| # of Months to Sell or Refi | 3 months | 6 months | 9 months | 12 months |

|---|---|---|---|---|

| Total Interest Estimate, Sum of Monthly Payments ($): | ||||

| Output: Up Front Loan Costs: | ||||

| Output: Up Front Appraisal and 3rd Party Fees: | ||||

| Total Up Front Loan Cost including 3rd Party ($): | ||||

New Construction Loan Process

Step 1- Initial Discussion, Loan Application, and Term Sheet

- Discuss the loan scenario including rehab construction plan, costs, and end value

- Suggest relevant loan programs and provide parameters

- Scope of Work form and recent experience schedule (we can get this over the phone too)

- Loan application and initial info request (we can get this over the phone too)

- Term Sheet and Appraisal Fee

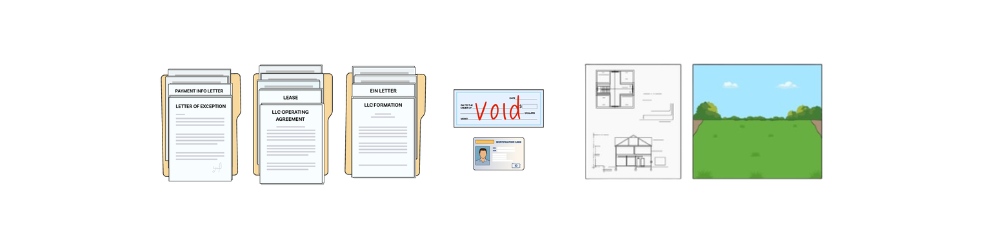

Step 2- Initial Info Required for New Construction Loan

- Any remaining info points to complete the Loan Application

- Photo of ID and void check

- Contact information for your title agent and insurance agent

- If borrower is an LLC, then LLC Operating Agreement and EIN Letter

- Bank statements with cash to close and required reserves for Purchases

- Building Plans

- List of permits needed

- Copies of any permits obtained (if available)

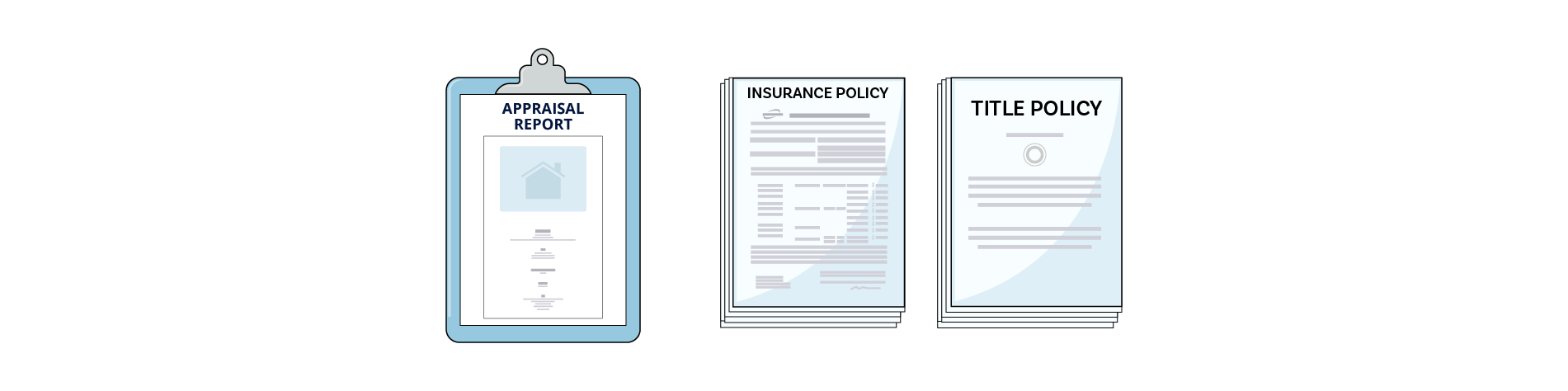

Step 3- Appraisal, Title, Insurance, and Additional Info from Borrower

- Appraiser visits the property and completes the appraisal report

- Lender reviews the appraisal report, internally re-checks value and reviews for property condition

- Title agent provides title policy, works with lender on revisions and clarifications

- Insurance agent provides insurance policy, works with lender on revisions and clarifications

- Lender usually comes up with other things to ask for from borrower

Step 4- Final Underwriting, Closing, and Funding

- Lender sends complete file to underwriting, and they may find issues or require more things at that point

- Final coordination between title company and lender on loan docs and scheduling

- Closing and Funding

What are Nonbank New Construction Loans?

Nonbank new construction loans are essentially fix n flip loans for new construction- private debt for building new construction homes. Larger and more established local homebuilders typically have relationships with banks and a lower cost of capital. Banks have more extensive requirements for income, assets, and experience requirements. Since 2008, banks have been more conservative on ground up bridge loans, and the private lenders have filled in for this niche.

Why do New Construction Loans have more borrower level requirements than Fix N Flip loans?

If a borrower can’t make it on a new construction ground up project, it is more difficult for a lender to work out a partly built house than it is for a house that is already built and just needs repairs. For this additional risk, lenders have more stringent loan-to-cost requirements and experience requirements for New Construction Loans than they do for Fix N Flip Loans.

Why do New Construction Loans take longer to close and cost more than Fix N Flip loans?

For new construction loans, lenders take more effort to vet the approvals, contractor/developer performing the work, project scope and budget, and value, due to the additional risk of new construction loans compared to fix n flip loans. Due to the additional risk and underwriting challenges, a new construction loan costs a bit more, and takes a bit longer to close, than a Fix N Flip loan. Private debt for new construction takes 20-30 days to close.

Are New Construction Loans available for Townhome and Condo Projects?

Yes, the same private lenders we use for single family home construction also lend on townhome and condo projects.

Are New Construction Loans available for Teardowns?

Yes, and the same loan-to-cost parameters apply for teardowns.

Are New Construction Loans available for Build for Rent, or just Build For Sale

New construction loans are available for both build for rent and build for sale scenarios. We are set up for both. The build for rent still needs to comp out as a for sale project.

Is there minimum interest for New Construction Loans?

There is usually no minimum interest and no interest charged on undrawn amounts. However, New Construction Loans have up front points and closing costs, and some lenders have minimum interest requirements.

Is a New Construction Private Loan the same as hard money for New Construction?

New Construction Private Loan is essentially hard money for new construction. The only other programs we have with interest rates as high as New Construction Loans are Fix N Flip Loans with the highest leverage, DSCR loans for commercial use property at the highest leverage, and DSCR loans on 1-4 unit residential and multifamily for borrowers with lower FICO scores.

Larger and more established local homebuilders typically have relationships with banks and a lower cost of capital. Banks have more extensive income, asset, and experience requirements but some of them are set up to meet the needs of qualified local builders. Historically, prior to 2008, banks were more involved in homebuilding loans. Since 2008, the banks have been more conservative on ground up bridge loans, and the private lenders have filled in for this niche.

Why do New Construction Loans have more borrowers level requirements than Fix N Flip loans?

If a borrower can’t make it on a new construction ground up project, it is more difficult for a lender to work it out on a mid project ground up than it is for a house that is already built and just needs repairs. For this additional risk, lenders have more stringent loan-to-cost requirements and experience requirements for New Construction Loans than they do for Fix N Flip Loans.

Why do New Construction Loans take longer to close and cost more than Fix N Flip loans?

For new construction loans, lenders take more effort to vet the approvals, contractor/developer performing the work, project scope and budget, and value, due to the additional risk of new construction loans compared to fix n flip loans. Due to the additional risk and underwriting challenges, a new construction loan costs a bit more, and takes a bit longer to close, than a Fix N Flip loan. New construction private loan takes 20-30 days to close.

Are New Construction Loans for individuals or LLCs?

For new construction loans, our lenders lend to individuals or LLCs in most states.

What are good questions to ask a New Construction Lender?

Ask a construction lender about their borrower experience requirements for new construction, how much of their practice is ground up construction lending, and what they do early in the process to evaluate deals and flag potential issues before sending a complete loan file to underwriting. Nonbank Clearing is a new construction loan specialist and we can underwrite the deal internally before even sending to lenders.

Nonbank Clearing Advantages

- Familiar with homebuilder scenarios and structures

- Competitive on rates, leverage, service, and handling draws

- Multiphase development and mid-project financing specialist

- Quick approval for new spec outside of existing credit lines

- Accommodate build to sell or build to rent strategy