Trustindex verifies that the original source of the review is Google.

Rick contacted me out of the blue one day because he saw all of the properties I was buying in the Philly area. I gave him a shot to refi one of my single family rentals. I was surprised how smooth the deal went. Lived up to everything he promised. I will def use him again for future DSCR loans.

Posted on

Darryl Miller

Trustindex verifies that the original source of the review is Google.

My experience with Nonbank Clearing was excellent due to Rick Bagel. He was informative and efficient. He was able to get me answers expeditiously. I was able to close on my loan in the allotted timeframe he gave me. He showed for closing and made sure everything went smoothly.

Posted on

Stay Focused

Trustindex verifies that the original source of the review is Google.

Working with Nonbank Clearing for my cash-out refi deal was a great experience. Specifically, working with Rick made the entire process easy and straightforward. He was incredibly detailed in his explanations, and I found their interest rates to be competitive, which was a huge plus. What really stood out was that it felt like a true partnership; he provided me with multiple options and walked me through the pros and cons of each. His clear and direct communication made the process feel transparent and efficient, and I felt like I was getting a good deal. I would highly recommend Nonbank Clearing!

Posted on

Xuan Nguyen

Trustindex verifies that the original source of the review is Google.

Rick was helping me with the loan so quickly, smooth and really professional . I will be back with him for the next loan . 5 stars I recommended

Posted on

Kinga Pokigo

Trustindex verifies that the original source of the review is Google.

Working with Rick was truly a game changer! I came to him with a sticky home situation in NJ and wasn’t sure there was even a path forward but Rick made the impossible happen. He not only secured me a fantastic loan, but did so with a level of dedication and professionalism that’s incredibly rare in the lending world!

Rick is extraordinarily responsive, transparent, and genuinely invested in helping his clients succeed. He took the time to understand my goals, walked me through every step, and made a stressful process feel manageable....even exciting. :D

A year later, I still recommend him to everyone I know & talk about that time. :) If you’re looking for someone who is knowledgeable, reliable, and will go the extra mile (and then some), Rick is totally your guy. You won’t find better! (Promise!)

Posted on

Brett B

Trustindex verifies that the original source of the review is Google.

Rick help me secure a DSCR loan for a rental property in NH. The transaction was smooth and Rick helped in every step along the way. I'll be using him again.

Posted on

Jaydon Barg

Trustindex verifies that the original source of the review is Google.

Great rates and very fast closing. Rick is the best!

Posted on

Anthony Blackmon

Trustindex verifies that the original source of the review is Google.

Rick is incredibly knowledgable. He helped me purchase an investment property. I'll be using him for many more transactions.

Posted on

Dan Hrubes

Trustindex verifies that the original source of the review is Google.

I have worked with Rick a handful of times with a customers refinancing of several investment properties. He has always been professional and very easy to work with, I would highly recommend Rick and his team.

Posted on

James Goett

Trustindex verifies that the original source of the review is Google.

My experience with Nonbank Clearing has been nothing but professionalism with no unforeseen changes in the process and a smooth closing on my refinance. I would recommend this team without reservation for your real estate financing needs.

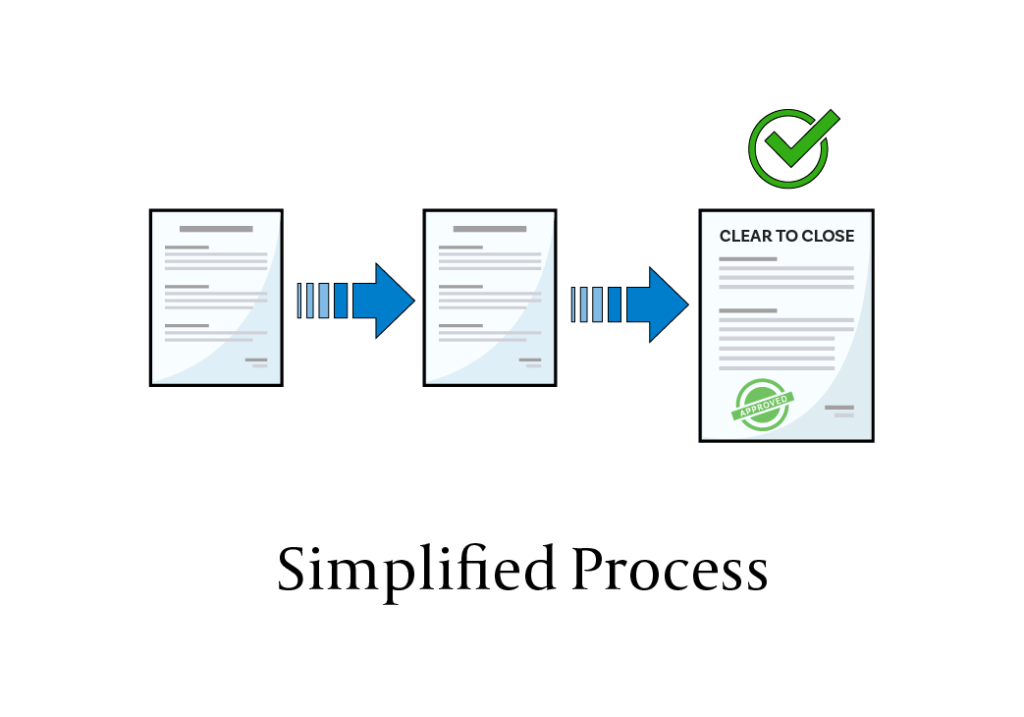

Nonbank Clearing Process

Before Application

Discuss the deal and figure out the right loan program, sizing, parameters, and approximate terms.

Loan Application

Provide information over the phone, or on a fillable form, along with supporting documentation.

Loan Approval

Approve lender terms and order appraisal.

Loan Processing

Work with Nonbank Clearing to meet simplified lender requests including LLC documentation, Title, Insurance, and property / project level info. The lenders usually come up with more info requests.

Loan Closing

Nonbank Clearing and lender partners coordinate with Closing Agent, Insurance Agent, Real Estate Agents, Borrower / Client, and anyone else needed, to get the loan clear to close and schedule closing.