- Compare bank and private lender options

- Cover wide range of property types

- Close loans outside of commercial banks

We have private debt and bank loan products available for commercial real estate loans and mixed use loans. The private lenders are bullish on housing, and they don't have the same excitement for commercial. For these loans, the banks are much more competitive on pricing. The private lender loans would only be used for convenience, speed, or because a bank said no. For mixed use properties that have > 50% of square footage residential, the private loan products open up a bit. Compare bank and nonbank commercial real estate loans with Nonbank Clearing !

What is a Commercial Real Estate Loan?

Multifamily properties, and 1-4 unit residential investment properties, are within the realm of commercial real estate lending. When we refer to “Commercial DSCR loans” or “Commercial Term Bank Loans” we mean loans against property with commercial use, such as office, retail, warehouse, industrial, or automotive.

In addition to banks and private lenders, there are life insurance companies, CMBS, and various other lender types for commercial real estate loans.

How to Qualify for a Commercial Real Estate Loan?

Call 609-468-9324 or email [email protected] and we can provide information on available bank and nonbank programs. Same day preapproval, and 1-2 day approval for no doc commercial loans. Longer timeline for bank loan approval. Hope to earn your business!

Commercial DSCR Loans vs. Commercial Term Bank Loans

| Commercial DSCR Loan | Commercial Term Bank Loan | |

|---|---|---|

| Term | 30 years | 5, 20, 25, or 30 years |

| Income and asset verification | No doc loan | Full income and asset verification required |

| Seasoning for cash out refi | 6 months | 6-24 months |

| DSCR Requirement | Varies, as low as 1.00 with 30 year amortization | Typically 1.20-1.25 with 20 or 25 year amortization |

| LTV Requirement | 65-75% cash out refi 70-80% purchase |

65-70% cash out refi 70-80% purchase |

| Time To Close | 30 days | 40-60 days |

| Rates, Points and Fees | Higher rates, these are some of | Lowest rates available |

| Payment Escrows | Monthly payments include tax and insurance escrow | Taxes and insurance paid outside monthly payments |

| Occupancy Requirement | 70% | 70% |

| Minimum FICO Score | 620-680 minimum | 620-680 minimum |

| Rehab Budget | None | None |

Commercial DSCR loans have the highest interest rates for any of the term loans we offer, except for 1-4 unit residential DSCR loans for borrowers with low FICO scores. The commercial DSCR interest rates get slightly better if you can settle for 50% of appraised value instead of full 65-75 LTV loans which have the highest interest rates.

| Commercial DSCR Loan Sweet Spots | Commercial Term Bank Loan Sweet Spots |

|---|---|

| ✅ DSCR loan allows for a cash out refi where a bank won’t meet on seasoning | 🏦 Bank already can meet on seasoning to approve requested cash out refi |

| ✅ Borrower not qualified for loan with full income and asset verification | 🏦 Borrower is qualified for a loan with full income and asset verification |

| ✅ Property is light on DSCR to meet full LTV requested | 🏦 Property meets more stringent bank loan DSCR requirements |

| ✅ Not a huge loan, where the convenience of a no doc loan is worth the additional interest | 🏦 Large loan, where the convenience of a no doc loan is not worth the additional interest |

| ✅ Quick close needed | 🏦 Borrower has all the time in the world to close a full doc bank loan |

Commercial DSCR is available for a wide range of commercial property types including automotive shops without underground storage tanks.

While no DSCR loans are available for a property where the owner resides personally, Commercial DSCR loans are available for both owner occupied businesses and properties that are leased.

Commercial Bank Term Loan Calculator

Bank loans for multifamily and commercial property are full doc loans, meaning they require 2 years personal and business income history, and the bank will verify assets (e.g. cash, stock, retirement plans, and other real estate owned). Unlike DSCR loans, banks typically do not escrow for property taxes and property insurance, so the monthly payment is just Principal and Interest (PI), as opposed to a DSCR loan payment which is Principal, Interest, Taxes, and Insurance (PITI). Typical amortization terms for bank loans are 20 years (240 months) and 25 years (300 months).

Up Front Costs

Bank loans have more stringent DSCR requirements than DSCR lenders.

Commercial DSCR Loan Calculator

Almost all DSCR loans are 30 year term, so we’ve plugged in 360 months for the term length.

For 1-4 unit residential, multifamily, and commercial / mixed use DSCR loans, the lenders escrow the estimated monthly cost for property taxes and property insurance. The monthly payments are PITI (Principal + Interest + Taxes + Insurance), like a 30 year home loan, even though these are commercial loan products.

Up Front Costs

In choosing a DSCR lender, rates, points, and fees are important, but equally important are service, reliability, and not finding a lender that bids low to win loans and re-trades later.

DSCR lenders have less stringent dscr criteria than bank lenders. DSCR loans for 1-4 unit residential properties do not require leases or occupancy, and lenders can go off market rate for rents. DSCR loans for multifamily, mixed use, and commercial, typically require 70% occupancy. The usual dscr requirement for a DSCR loan is 1.00, based on rents divided by the PITI monthly payment with 30 year amortization, and we have lenders that can work with 0.75-0.99 dscr for certain scenarios. A full doc bank loan would adjust rental income downward for operating expenses and vacancy (not just taxes and insurance) and require 1.20 or 1.25 dscr at 20 or 25 year amortization.

Commercial Loan Process

Step 1- Initial Discussion, Loan Application, and Term Sheet

- Discuss the loan scenario including rehab construction plan, costs, and end value

- Suggest relevant loan programs and provide parameters

- Scope of Work form and recent experience schedule (we can get this over the phone too)

- Loan application and initial info request (we can get this over the phone too)

- Term Sheet and Appraisal Fee (if required)

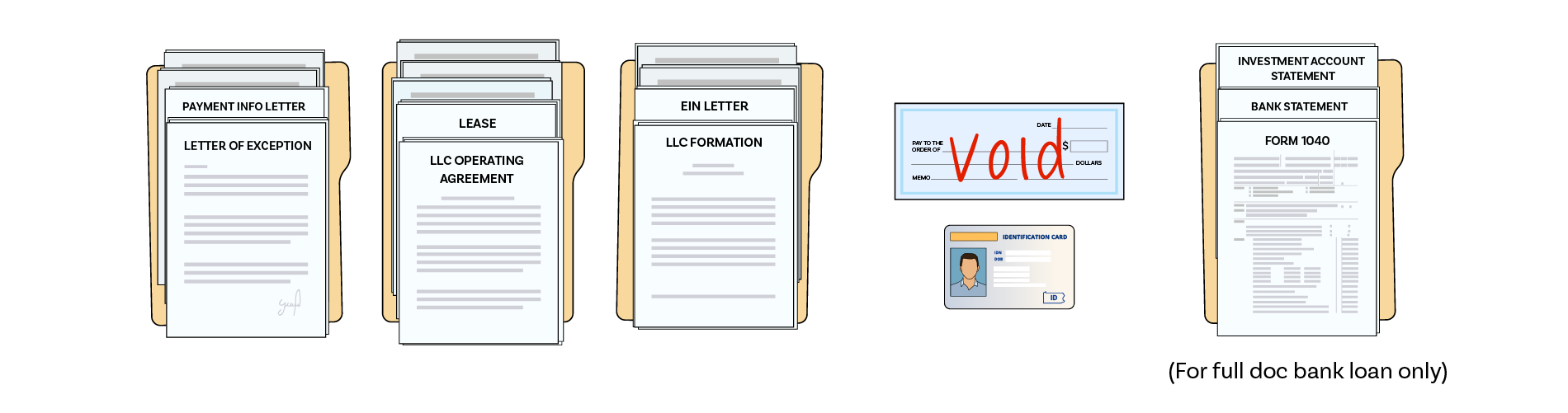

Step 2- Initial Info Required for Commercial Loan

- Loan Application and Appraisal Fee if required (see previous step)

- Photo of ID and void check

- Contact information for your title agent and insurance agent

- If borrower is an LLC, then LLC Operating Agreement and EIN Letter

- Bank statements with cash to close and required reserves

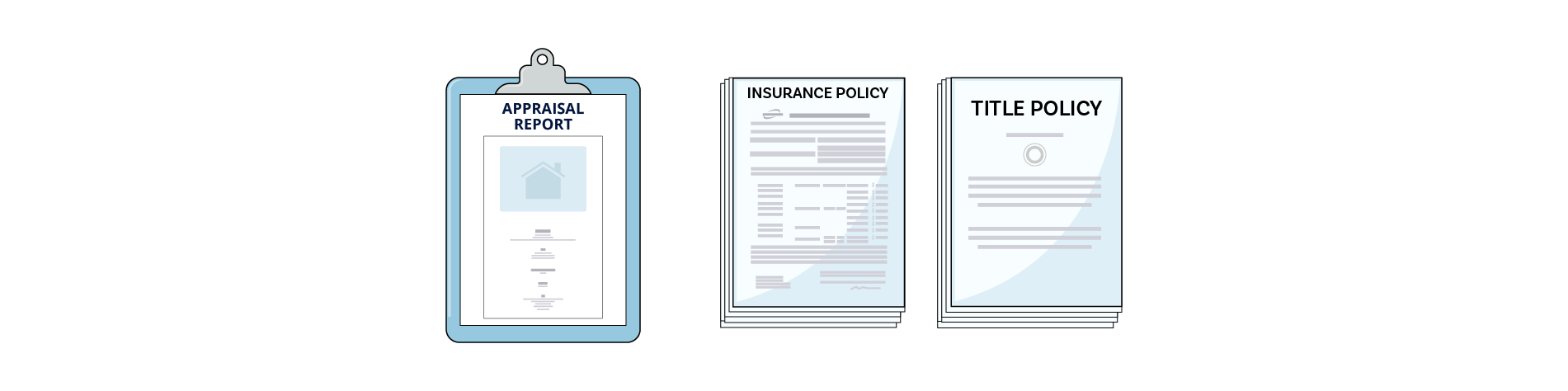

Step 3- Appraisal, Title, Insurance, and Additional Info from Borrower

- Appraiser visits the property and completes the appraisal report or borrower submits photos for lender (for our lenders that do desktop appraisal).

- Lender reviews the appraisal report, internally re-checks value and reviews for property condition, or completes internal valuation (desktop appraisal).

- Title agent provides title policy, works with lender on revisions and clarifications

- Insurance agent provides insurance policy, works with lender on revisions and clarifications

- Lender usually comes up with other things to ask for from borrower

Step 4- Final Underwriting, Closing, and Funding

- Lender sends complete file to underwriting, and they may find issues or require more things at that point

- Final coordination between title company and lender on loan docs and scheduling

- Closing and Funding

Commercial DSCR Loan vs. Commercial Term Bank Loan Requirements

Most of the requirements for Commercial DSCR loans and Commercial Term Bank Loans are outlined in the graphic above. If you are getting your stuff together to apply for a Commercial DSCR loan or Commercial Term Bank Loan, please be ready to meet the following requirements:

- Loan Application

- Schedule of Real Estate Owned

- LLC documents including Operating Agreement (if applicable)

- Title Policy meeting lender requirements

- Insurance Policy meeting lender requirements

- Leases

- Last 12 months and projected Operating Expenses

- Purchase contract (if purchase)

- HUD1 from purchase (if purchased recently)

- Summary of work completed at the property (if applicable)

- Completed appraisal (ordered by lender, paid for by borrower)

- Environmental study (usually required)

- No income verification required for Commercial DSCR Loan

- 2 years business and personal income, and asset verification, required for Commercial Term Bank Loan

DSCR Loans for Mixed Use Property with > 50% sq footage Residential

Mixed Use DSCR loans, for mixed use property where more than 50% of the square footage is residential, usually has a lower interest rate than Commercial DSCR loans.

Private Bridge Loans for Commercial and Mixed Use Property

We offer private bridge loans for commercial and mixed use property. These loans all require investment experience.

| Private Bridge Loan Commercial | Private Bridge Loan Mixed Use > 50% SF Residential | |

|---|---|---|

| Loan Amount | $250k+ | $250k+ |

| Loan Term | 12-24 months | 12-24 months |

| Max Leverage | Up to 65% of purchase price + 100% of construction hard cost | Up to 75% of purchase price + 100% of construction hard cost |

| Time to Close | 30 days | 30 days |

| Borrower Income and Asset Verification, DTI | No doc loan | No doc loan |

| Experience Required | Yes | Yes |

| Rates, Points and Fees | Private bridge rates | Private bridge rates |

| LTARV requirement | 65% | 70% |

| Minimum FICO Score | 680 | 680 |

Nonbank Clearing Advantages

- Compare bank and private lender options

- Cover wide range of property types including warehouse and automotive

- We can help close loans that commercial banks are not funding