Frequently Asked Questions

14-21 calendar days. Fix n flip

20-30 calendar days. DSCR, vacation rental, multifamily, commercial, mixed use

30-60 calendar days. Full doc bank loan for multifamily, commercial, or mixed use

For multifamily (5+ unit residential), mixed use, and commercial, you would need 70% of the property leased to get a refi, and we could either look at the private lenders at higher leverage, quicker close, and higher rate, or the banks to get a regular full doc bank loan.

Loan Calculators

DSCR Loan Calculator

Almost all DSCR loans are 30 year term, so we’ve plugged in 360 months for the term length.

For 1-4 unit residential, multifamily, and commercial / mixed use DSCR loans, the lenders escrow the estimated monthly cost for property taxes and property insurance. The monthly payments are PITI (Principal + Interest + Taxes + Insurance), like a 30 year home loan, even though these are commercial loan products.

Up Front Costs

In choosing a DSCR lender, rates, points, and fees are important, but equally important are service, reliability, and not finding a lender that bids low to win loans and re-trades later.

DSCR lenders have less stringent dscr criteria than bank lenders. DSCR loans for 1-4 unit residential properties do not require leases or occupancy, and lenders can go off market rate for rents. DSCR loans for multifamily, mixed use, and commercial, typically require 70% occupancy. The usual dscr requirement for a DSCR loan is 1.00, based on rents divided by the PITI monthly payment with 30 year amortization, and we have lenders that can work with 0.75-0.99 dscr for certain scenarios. A full doc bank loan would adjust rental income downward for operating expenses and vacancy (not just taxes and insurance) and require 1.20 or 1.25 dscr at 20 or 25 year amortization.

Hard Money Loan Calculator

Fix n flip loans and New construction loans are typically 12 month, 18 month, or 24 month balloon loans, interest only, where the borrower intends to repay the loan by either refinancing (taking out) the bridge loan with a permanent loan, or selling the property and repaying the loan at sale.

The “Rehab Holdback Use Factor” is a simplification to help estimate the total monthly interest payments. Our lenders typically don’t charge interest on undrawn amounts, so we’ve included this percentage to adjust for not using the entire rehab holdback amount from the beginning of the loan. Our lenders typically have no minimum term length. They get you on the up front points and fees and then the total interest paid is variable depending on how soon you draw the money and how many months until you pay it back, with no minimum interest.

| # of Months to Sell or Refi | 3 months | 6 months | 9 months | 12 months |

|---|---|---|---|---|

| Total Interest Estimate, Sum of Monthly Payments ($): | ||||

| Output: Up Front Loan Costs: | ||||

| Output: Up Front Appraisal and 3rd Party Fees: | ||||

| Total Up Front Loan Cost including 3rd Party ($): | ||||

For a fix n flip example, $250k purchase price and $50k rehab budget, you could model 85% of the purchase price for purchase loan amount ($250,000 x 85% = $212,500) and $50,000 for the rehab holdback amount (rehab budget).

For a new construction loan example, with $50k lot cost and $250k project budget to build a house, you could model $50k down to pay for the lot in cash and then borrow $250k rehab holdback amount, so $0 purchase loan amount and with $250,000 rehab holdback amount.

Terms and leverage parameters vary for fix n flip loans and new construction loans. Call us to check your assumptions 609-468-9324.

Multifamily and Commercial Bank Loan Calculator

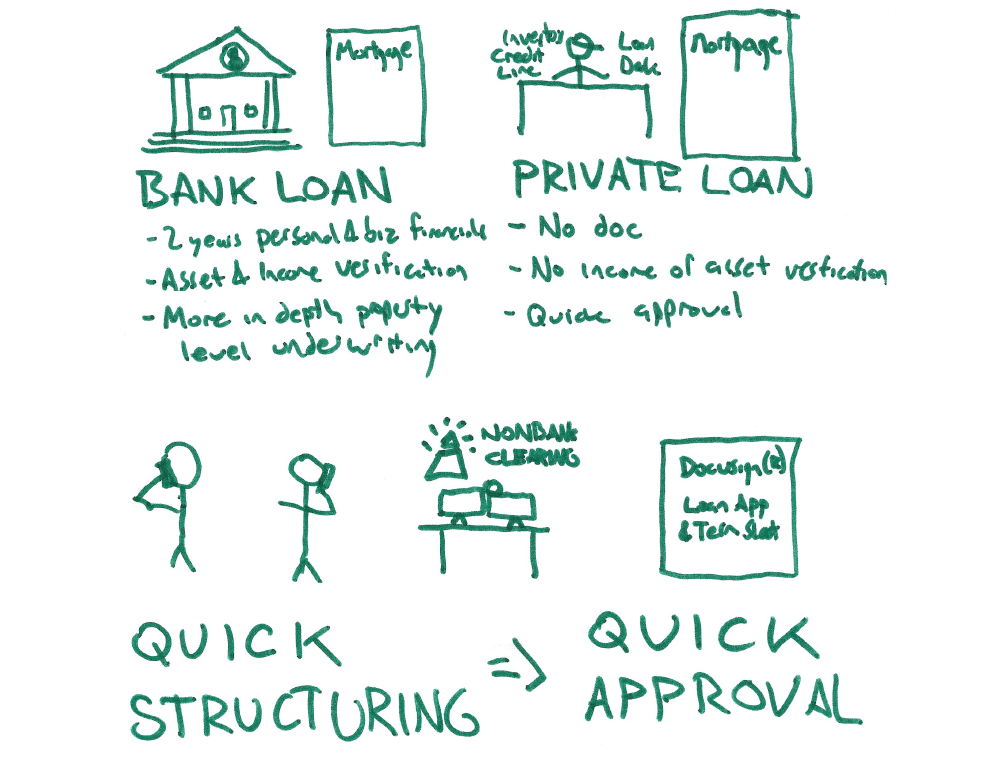

Bank loans for multifamily and commercial property are full doc loans, meaning they require 2 years personal and business income history, and the bank will verify assets (e.g. cash, stock, retirement plans, and other real estate owned). Unlike DSCR loans, banks typically do not escrow for property taxes and property insurance, so the monthly payment is just Principal and Interest (PI), as opposed to a DSCR loan payment which is Principal, Interest, Taxes, and Insurance (PITI). Typical amortization terms for bank loans are 20 years (240 months) and 25 years (300 months).

Up Front Costs

Bank loans have more stringent DSCR requirements than DSCR lenders.

Glossary

What is DSCR?

Debt Service Coverage Ratio (DSCR) is a generic finance term for business cash flow as a proportion of debt service. It is not just for real estate finance.

If an online store has $15k / month income before debt service and it has loan payments of $10k / month then that loan has a debt service coverage ratio of 1.50.

If a rental property has $12k / month in actual rents and the mortgage payment on that property is $10k / mo including escrows for taxes and insurance, then that loan has a debt service coverage ratio of 1.20, assuming lender doesn't subtract for vacancy loss and operating expenses.

What is a DSCR loan?

The DSCR loan, also known as the long term rental loan, short term rental loan, ltr loan, str loan, and 30 year no doc loan, usually refers to the 30 year no doc loan for 1-4 unit residential rental properties with no income verification. The lenders syndicate these loans to investors who issue bonds, and there is a market for the bonds like RMBS or CMBS.

There are other DSCR loan programs, for multifamily, commercial, and mixed use properties. These loans are with private lenders and they don't require personal or business income verification. Generally, the multifamily and mixed use with > 50% square footage residential DSCR loans have a little higher interest rate than the 1-4 unit residential, and they have occupancy requirements. The commercial and mixed use > 50% square footage commercial DSCR is priced even higher but it works sometimes on convenience or if the bank doesn't want to do it.

Do DSCR loans require leases or occupancy?

For 1-4 unit residential properties, they do not require leases or occupancy. For other property types, the no doc / DSCR loans usually require the property to be at least 70% leased.

What is a Fix N Flip loan?

The Fix N Flip loan, also known as the fix and flip loan, fix n flip bridge loan, and rehab bridge loan, usually refers to a purchase and rehab bridge loan for a 1-4 unit residential property with a 12 or 18 month term.

Purchase and rehab bridge loans for multifamily, mixed use, and commercial properties could be called fix n flip loans, multifamily bridge loans, fixed use bridge loans, and commercial bridge loans.

What is the difference between a DSCR loan and a fix n flip loan?

DSCR loans for 1-4 unit residential are syndicated on the bond market and have a lower interest rate.

Can I use a DSCR loan for a bridge scenario?

You can, but DSCR loans are only for rented or rent ready properties, and there is either a prepayment penalty, a higher interest rate to buy out the prepayment penalty, or points up front to buy out the prepayment penalty.

What is a new construction loan?

A new construction loan, also known as a ground up loan, or ground up construction loan, is a purchase and rehab bridge program for building a new single family house, 2-4 family house, or a phase of houses with a 12 or 18 month term.

What is a hard money loan?

Hard money loan is another word for private bridge loan, so fix n flip, new construction, or any bridge program that is from a private lender and not a bank.

What makes it 'hard' is that it is short term (12 or 18 months), and it is from a private lender, so the rates are higher than bank rates.

Do hard money loans fund purchase and renovation?

Yes. The loan amount includes a rehab holdback which gets drawn out to borrower as work is completed on the property. Our lenders won't extend draws for materials or appliances- they go off the budget you send, and the percentage completed on site for each line item at the time they inspect.

What is a private lender?

A private lender is any lender that is not a bank, credit union, insurance company, or institution. Private lenders are also known as nonbank lenders or non-bank lenders.

What is a commercial loan?

Commercial loan is a generic term for any loan to a business. Business credit cards, equipment loans, commercial real estate loans, and even the DSCR and fix n flip products are all types of commercial loans.

Sometimes people refer to a 'full doc' loan from a bank as a commercial loan. These loans requires 2 years of personal and business financials and asset verification, in addition to the property level underwriting.

What is the BRRR method?

BRRRR or BRRRR method stands for 'buy, rehab, rent, refinance, repeat'. It is also known as BRRR or BRRR method, which stands for 'buy, rehab, rent, refinance'. It means buying property for cash or with a fix n flip loan, fixing up the house and/or raising the rents, and refinancing instead of selling. Our brokered loan products go hand in hand with the BRRRR method.

What is LTV?

LTV stands for 'Loan To Value'. LTV is the loan amount divided by the value of a property. For a purchase scenario, value is considered the lower of the purchase price and the appraised value. For a refi, assuming seasoning requirement is met, value is just the appraised value.

What is LTC?

LTC stands for 'Loan To Cost'. It is the loan amount divided by the purchase price of the property plus hard cost of any improvements. For a project that is $200k purchase price, and $20k rehab budget, a 90 LTC loan would be $22k + closing costs from borrower and loan amount $178k towards purchase + $20k rehab holdback from lender. Lenders sometimes quote these at 85/100 or 90/100, which means the lender funds 85 or 90% of purchase, and 100% of rehab. For budgeting purposes, the down payment percentages never include closing costs or soft costs.